IFRS 15: Step 1 - Identifying a contract with a customer

AuditRead the second article in new Insights into IFRS 15 series – ‘Step 1: Identifying a contract with a customer.

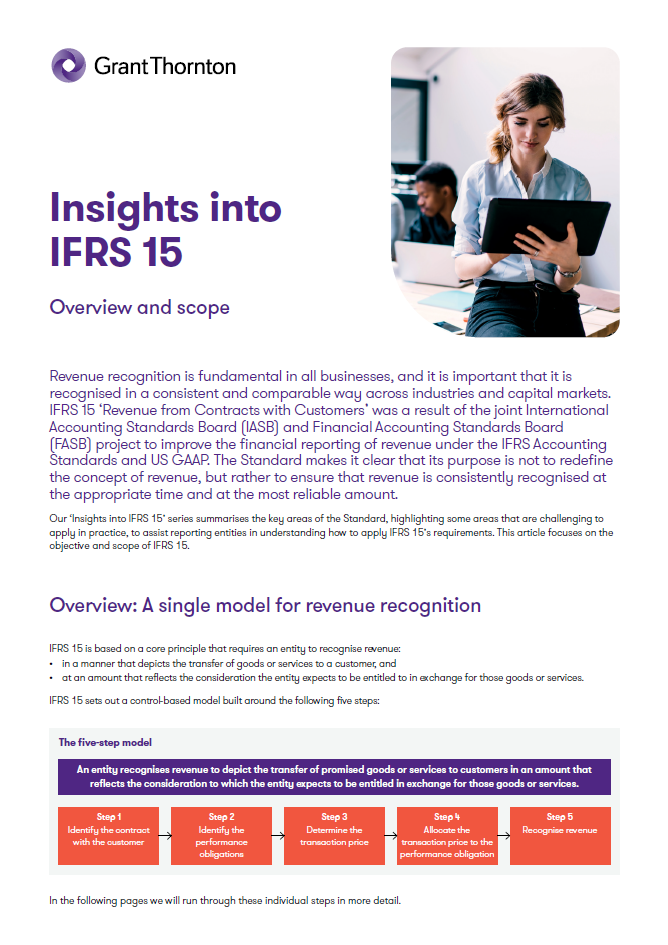

IFRS 15 ‘Revenue from Contracts with Customers’ was a result of the joint International Accounting Standards Board (IASB) and Financial Accounting Standards Board (FASB) project to improve the financial reporting of revenue under the IFRS Accounting Standards and US GAAP (Generally Accepted Accounting Principles). The Standard makes it clear that its purpose is not to redefine the concept of revenue, but rather to ensure that revenue is consistently recognised at the appropriate time and at the most reliable amount.

Our ‘Insights into IFRS 15’ series summarises the key areas of the Standard, highlighting some areas that are challenging to apply in practice, to assist reporting entities in understanding how to apply IFRS 15’s requirements. This article focuses on the objective and scope of IFRS 15.

Download this article for a full insight into the overview and scope of IFRS 15, including detailed examples and practical insights.

Read the second article in new Insights into IFRS 15 series – ‘Step 1: Identifying a contract with a customer.